Grafted Polyolefins Market Outlook 2024–2033

- James Anderson

- May 18

- 4 min read

Market Overview

The global Grafted Polyolefins Market is projected to reach USD 1.9 billion in 2024 and is expected to grow further to USD 2.9 billion by 2033, registering a CAGR of 5.0% over the forecast period 2024–2033.

Grafted polyolefins are chemically modified polymers formed by attaching functional groups onto base polyolefins such as polyethylene and polypropylene. This modification enhances their interfacial adhesion, compatibility, and overall performance, making them suitable for applications in automotive parts, packaging materials, adhesives, and polymer compounding. Their strong ability to improve bonding between different materials has made them highly valuable in advanced industrial applications.

The market expansion is being driven by increasing demand from automotive and packaging industries, where there is a strong need for lightweight, durable, and high-performance materials. Additionally, rising usage in wire and cable insulation along with growing applications in engineered plastics is further supporting market growth. Continuous improvements in polymer grafting technologies are also enhancing product efficiency and expanding application scope.

Definition and Market Significance

Grafted polyolefins are functional polymers created through grafting processes that introduce reactive chemical groups onto polyolefin chains. This structural modification improves adhesion between polymers and other materials such as metals, fillers, and polar resins.

The importance of this market is rooted in its ability to enhance material performance across multiple industries. It enables the production of advanced composites, high-performance packaging solutions, and lightweight automotive components, thereby supporting innovation in manufacturing and material engineering.

Market Drivers

One of the primary drivers of the grafted polyolefins market is the increasing requirement for lightweight and fuel-efficient materials in the automotive sector. Manufacturers are actively shifting toward advanced polymers to reduce vehicle weight and improve efficiency.

Growth in the packaging industry is also contributing significantly, particularly in flexible packaging applications that require strong sealing and adhesion properties.

Rising adoption in electrical and electronic applications, especially for insulation in wires and cables, is further accelerating market demand.

In addition, ongoing advancements in polymer modification and grafting technologies are improving material properties and expanding usage areas.

Market Trends

A notable trend in the market is the growing preference for high-performance engineered polymers with superior mechanical and thermal characteristics.

Sustainability-driven demand is increasing the use of grafted polyolefins in recyclable and eco-friendly packaging solutions.

The automotive industry’s focus on lightweighting strategies is also strengthening adoption of these materials to improve fuel efficiency and reduce emissions.

Moreover, advancements in reactive extrusion and grafting processes are improving production efficiency and product uniformity.

Market Restraints

Volatility in raw material prices, especially petrochemical-based inputs, can impact production costs and market stability.

The complex nature of grafting processes and high capital requirements may restrict adoption among small-scale manufacturers.

Environmental concerns related to plastic usage and tightening regulatory frameworks also pose challenges to market expansion.

Market Opportunities

Rapid industrialization in emerging economies is creating strong opportunities for market growth.

Increasing investments in sustainable and recyclable polymer technologies are expected to support innovation and new product development.

The expansion of electric vehicles and demand for lightweight automotive components are also generating significant growth prospects for grafted polyolefins.

Segmentation

The grafted polyolefins market is categorized based on type, application, and end-use industry. Maleic anhydride grafted polyolefins hold a dominant position due to their strong compatibility and wide usage across industries.

In terms of application, adhesives and sealants represent a key segment driven by growing demand for high-strength bonding solutions.

The automotive and packaging industries remain the major end-use sectors, supported by increasing demand for lightweight and high-performance materials.

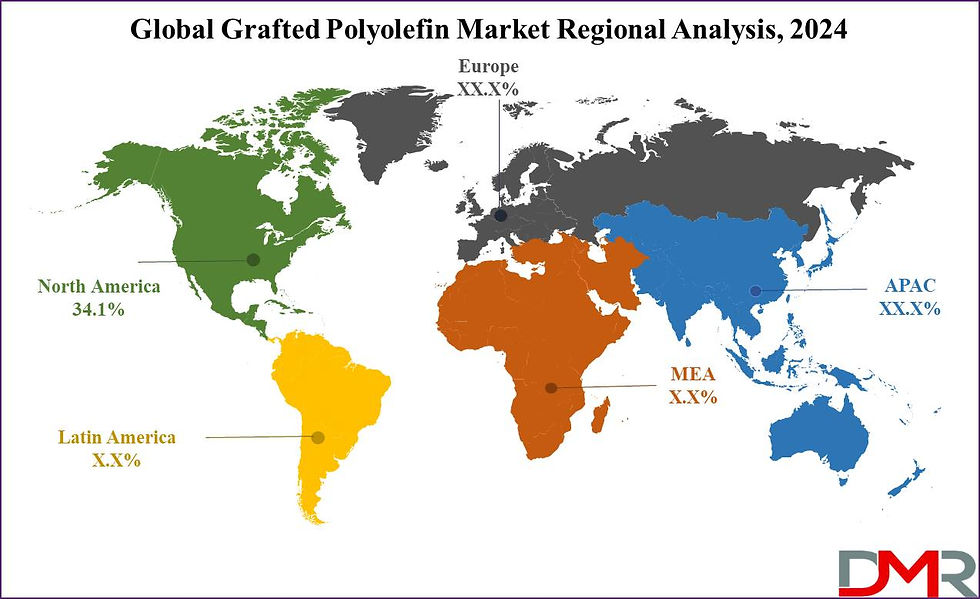

Regional Analysis

North America

North America leads the grafted polyolefins market with a revenue share of 34.1% in 2024. The region benefits from a strong industrial base, high disposable income levels, and advanced technological capabilities. Leading manufacturers are concentrated in this region and are actively investing in research and development to introduce innovative and high-performance solutions.

Europe

Europe holds a notable share of the market, supported by a well-established automotive industry and growing demand for sustainable material solutions. Strict environmental regulations are also encouraging the adoption of advanced polymer technologies.

Asia-Pacific

Asia-Pacific is expected to grow rapidly due to expanding industrial activities, increasing automotive production, and rising packaging demand in countries such as China and India.

Latin America

Latin America is witnessing steady expansion supported by growing manufacturing activities and increasing demand for automotive and packaging applications.

Middle East & Africa

The region is gradually adopting grafted polyolefins, driven by infrastructure development and rising industrial usage.

Download a Complimentary PDF Sample Report

Competitive Landscape

The grafted polyolefins market is moderately consolidated, with key players focusing on innovation, capacity expansion, and strategic collaborations. Major companies include Dow Inc., LyondellBasell Industries, Arkema Group, Eastman Chemical Company, and Borealis AG. Continuous investment in research and development remains central to strengthening product performance and expanding application areas.

Technological Advancements

Advancements in reactive extrusion and polymer grafting technologies are improving process efficiency, consistency, and functional properties of grafted polyolefins. Developments in catalysts and processing systems are further enhancing scalability and material performance.

Consumer Adoption Patterns

Adoption is increasing across automotive, packaging, and industrial sectors due to the material’s strong adhesion, compatibility, and lightweight characteristics. Demand is particularly high in applications requiring durability and enhanced mechanical performance.

Regulatory Environment

Regulatory frameworks focused on polymer sustainability, recyclability, and environmental impact are shaping product innovation. Manufacturers are increasingly aligning with global standards to ensure compliance and sustainability.

Market Challenges

Key challenges include fluctuating raw material prices, complex manufacturing processes, and environmental concerns associated with plastic materials. Addressing these issues is essential for long-term market stability.

Future Outlook

The grafted polyolefins market is expected to maintain consistent growth, supported by rising demand for advanced materials, expansion of automotive lightweighting initiatives, and increasing use in packaging applications.

FAQs

What is the grafted polyolefins market?

It refers to modified polyolefins produced through grafting techniques to enhance adhesion and performance.

What is the market size of grafted polyolefins?

USD 1.9 billion in 2024, projected to reach USD 2.9 billion by 2033.

What is the CAGR of the market?

5.0% during 2024–2033.

Which region dominates the market?

North America with a 34.1% share in 2024.

What are the key drivers?

Demand for lightweight materials, packaging growth, and advancements in polymer technology.

Summary of Key Insights

The grafted polyolefins market is showing stable expansion driven by rising demand for high-performance and lightweight materials across automotive and packaging sectors. North America remains the leading region, while Asia-Pacific offers strong future growth potential.

Purchase the report for comprehensive details

Comments